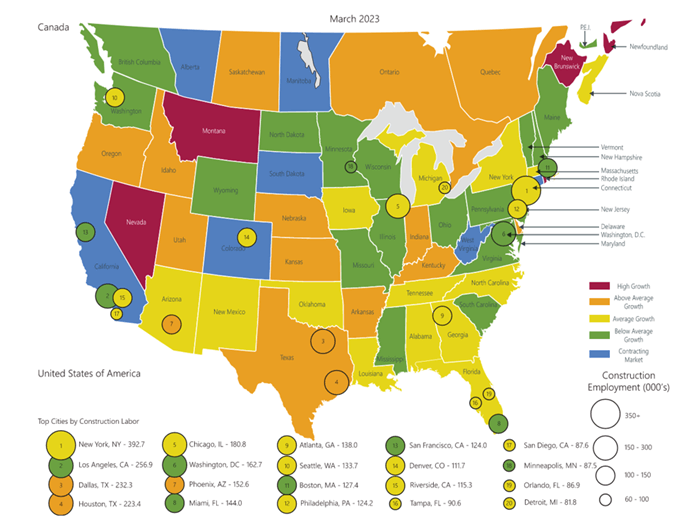

Market Outlook Quarterly Q1 2023

-

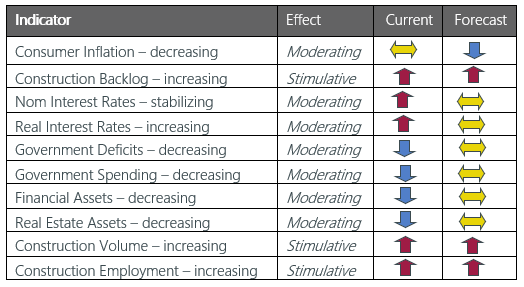

Ongoing increases raised interest rates to 5.25% in May along with continued quantitative tightening. This has caused a decrease in interest rate sensitive sectors such as residential construction

-

Short term construction price inflation is forecast to continue at 9% before settling toward 6% for 2023, 5% for 2024, then settling to a long-term average of 4%

-

Volatility remains high. We continue to recommend additional bidding contingencies in the 5 to 15% range for projects bidding in the near-term

-

Institutional-Commercial Construction Prices rose in Q1 of 2023 at 0.75% per month

-

Supply Chain Shortages, labor shortages, and increased backlogs have impacted bid prices. However, supply chain improvements and fear of recession have reduced the cost impact of these factors

-

Architectural Billings went up slightly at March end but continued down for the rest of Q1

-

Construction Dollar Volume: residential construction continued to decrease in Q1 by 0.85%; nonresidential construction is up 20.5% year to year; and infrastructure spending increased 2.43% this quarter

-

Construction Job Growth: approximately 29,000 construction jobs were added in Q1, or +0.37%; construction employment is now 3.7% above pre-pandemic levels

-

The New York Stock Exchange has dropped 9.13% year over year

-

Total Employment Growth through Q1 was 345,000 on average per month, well above recession levels

-

Gross Domestic Product: Growth for 2022 was 0.9%. Q1 2023 increased to an annual rate of 1.1%

-

Commodity prices continue to decline to long-term averages

Fed Watch

Inflation and Employment Targets propel monetary policy, and subsequently construction prices. Ongoing increases raised interest rates to 5.25% in May along with continued quantitative tightening. This has caused a decline in interest rate sensitive sectors such as residential construction.

“Over the 12 months ending in March, total PCE prices rose 4.2 percent. Inflation has moderated somewhat since the middle of last year. Despite elevated inflation, longer-term inflation expectations appear to remain well anchored, as reflected in a broad range of surveys of households, businesses, and measures from financial markets.” Chair Powell’s Press Conference May 3, 2023

“You want to be at a place where real interest rates are positive across the entire yield curve and measure those against some forward-looking assessment of inflation.”

“You want to be at a place where real interest rates are positive across the entire yield curve and measure those against some forward-looking assessment of inflation.”

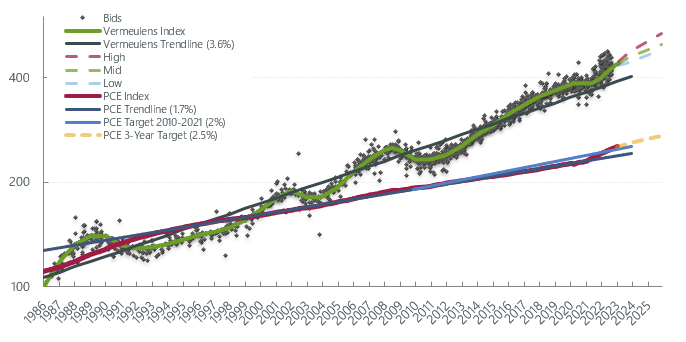

Vermeulens Construction Cost Index

Prices for Q1 2023 nationally increased 0.75% monthly as contractor backlogs filled, and labor/material shortages continued.

For the past 37 years, nonresidential construction prices trended at a 3.6% annually compounded escalation rate. The rate of escalation seen in construction costs relates to the target of 2% annual inflation for consumer prices and the monetary policy used to achieve this goal. Consumer inflation has increased rapidly above the long-term target of 2%.

In contrast to previous financial recessions, strong and immediate fiscal and monetary measures countered the collapse in activity at the outset of the pandemic. 2022 saw these measures reversing due to the overwhelming strength of major indicators. 2023 is expected to see a pause in further measures anticipating moderating prices and employment indicators.

Vermeulens Index tracks bid prices for nonresidential construction projects relative to the average represented by Vermeulens Trendline. Personal Consumption Expenditures Index tracks general prices relative to PCE Trendline and PCE Target. Strength in nonresidential construction point to short-term cost increases of 0.75% per month, and a continuing increase in the long-term Vermeulens Trendline toward 4%.

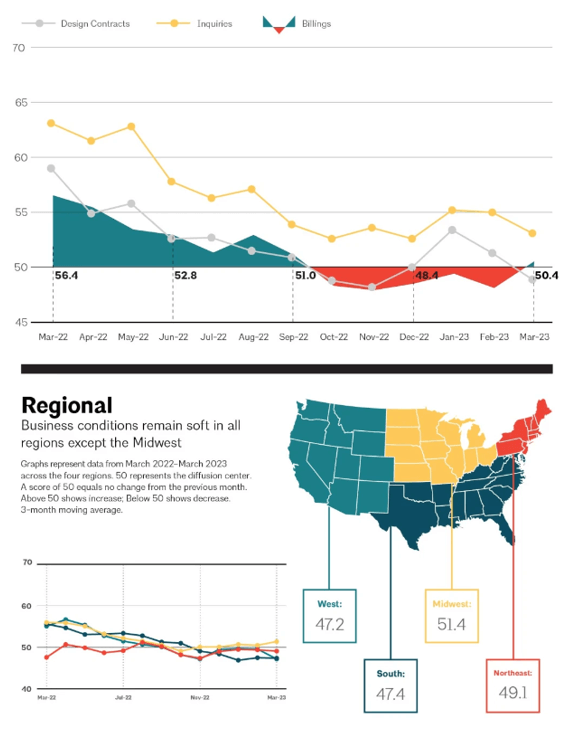

AIA Billings

Architectural Billings are a leading indicator for future construction volume. A score greater than 50 indicates growth. Design fee billings typically indicate construction volume 9 - 12 months in advance.

Architectural billings declined last quarter. The value of new signed design contracts also fell while inquiries grew slightly.

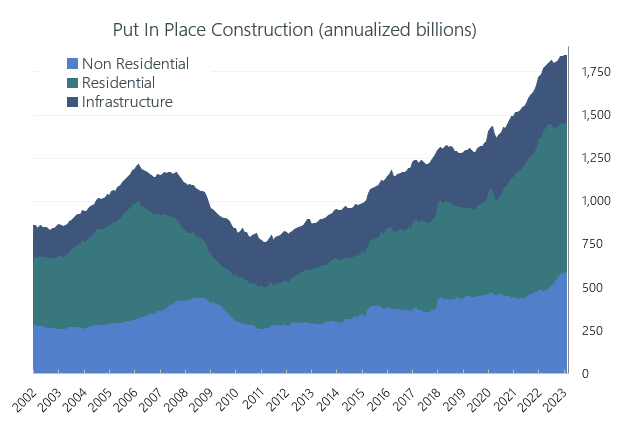

Put In Place Construction

Construction Dollar Volume grew by 0.21% in Q1, posting a 6.2% year-over-year increase (Feb 22/Feb 23). Construction dollar volume is the main driver of construction prices.

Residential dollar volume declined 0.85% in Q1, decreasing year over year by 2.7% (Feb 22/Feb 23).

Nonresidential spending is up 20.5% year over year (Feb 22/Feb 23). Improved backlogs, attrition, and shortages are driving price increases in this sector.

Infrastructure spending increased 2.43% in Q1 2023, with an 8.8% year-over-year change (Feb 22/Feb 23). Federal infrastructure spending will increase over the next 10 years. See Fiscal Watch for an impact assessment of new programs.

“We are seeing the effects of our policy tightening on demand in the most interest rate sensitive sectors of the economy, particularly housing, and investment.” Chair Powell’s Press Conference May 3, 2023.

http://www.census.gov/construction/c30/c30index.html

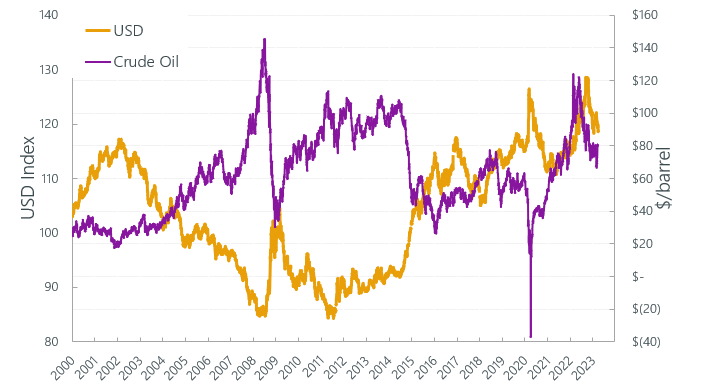

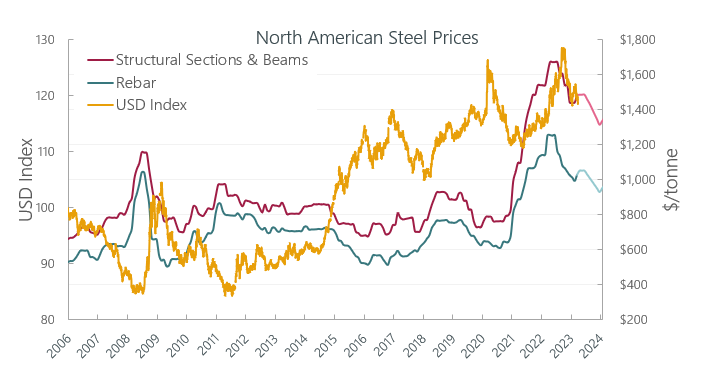

Commodity Prices

Supply chain shortages, labor shortages, and increased backlogs are impacting bid prices. However, the supply chain and fear of recession have reduced the cost impact of these factors.

Crude Oil reduced to $75.68 per barrel at the end of March 2023 from its peak of $123.64. Prices were volatile throughout the last quarter, peaking at $81.62 on January 23rd. Structural sections and beams decreased 3.06% and rebar is down by 0.20% since December 2022.

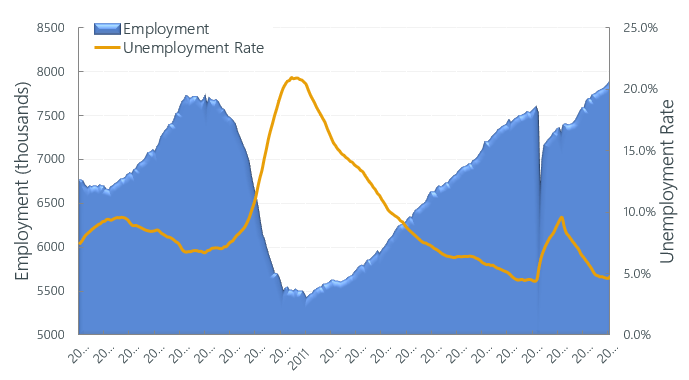

Construction Labor Market

Construction Unemployment at the end of Q1 sits at 5.6% (12-month average), up from 4.4% at the end of Q4 2022, reflecting lower growth in total construction dollar volume.

Construction Job Growth was 29,000 or 0.37%, this quarter. Wage and profit increases in the non-residential sector will draw new entrants, as well as restructuring from the residential sector and other sectors of the economy. Labor growth is likely to continue its steep rise as selling prices in the sector outperform other industries.

Construction Labor Force Growth Rate

Construction Labor Force Growth Rate is calculated by the current 12-month average in construction employment relative to the previous 12-month average in construction employment.

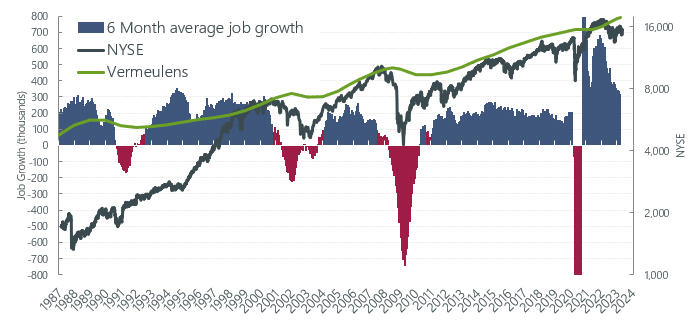

Total Jobs and Market Performance

Monthly Average Job Growth for the US economy through Q1 was 345K peaking in January with 472k before falling to 236k in March.

“Right now, you have a labor market that's still extraordinarily tight. You still have 1.6 job openings, even with the lower number of job openings for every unemployed person. We do see some evidence of softening in labor market conditions. But, overall, you're near a 50-year low in unemployment. Wage increases are a couple of percentage points above what would be consistent with 2 percent inflation over time. So, we do see some softening, we see labor supply coming in. These are very positive developments.” Chair Powell’s Press Conference May 3, 2023.

The chart below removes short-term fluctuations in job growth by looking at a 6-month moving average. The size of the labor force grows at 100,000 per month due to population increase. Sustained periods of recession, where job creation remains below 100,000 jobs per month, has accompanied dips in construction prices as illustrated by the red bars below.

https://data.bls.gov/timeseries/CES0000000001

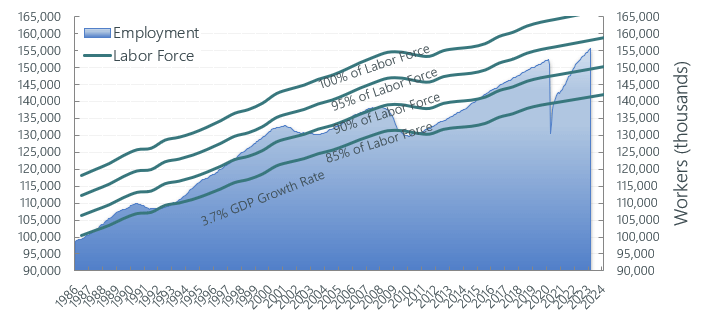

Employment Percentage of Total Workforce

Total Employment as a percentage of the total workforce continued its recovery reaching more than 94% at the end of Q1 2023. The chart below shows total employment as a percentage of the US workforce. The Federal Reserve will accommodate growth to maximize employment. Both the size of the labor force and participation rates are at play. Labor force growth has not kept pace with employment opportunities, resulting in shortages.

“I continue to think that it's possible that this time is different. And the reason is there's just so much excess demand, really, in the labor market.” Chair Powell’s Press Conference May 3, 2023.

Forecast - National Trend

Nonresidential Construction prices continued to rise in 2023 at 0.75% per month as they did through 2022. Contractor backlogs, strong margins, increased labor costs, and volatility in supply prices contributed to these rates. Short-term construction price inflation is forecast to continue at 9% for 2023, moderating to 5% for 2024, then settling to a long-term average of 4%. This aligns with Federal Reserve estimates for inflation of 5.6% for 2022, 3.6% this year, 2.5% in 2024, and 2.1% in 2025.

Volatility remains high. We continue to recommend additional bidding contingencies in the 5 to 15% range.

“It wasn't supposed to be possible for job openings to decline by as much as they've declined without unemployment going up. Well, that's what we've seen. It just seems to me that it's possible that we can continue to have a cooling in the labor market without having the big increases in unemployment that have gone with many prior episodes. Now, that would be against history. Despite excess demand, wage increases have been moving down to a more sustainable level.” Chair Powell’s Press Conference May 3, 2023.

Vermeulens strives to give our clients the greatest possible value and results for their projects. If you:

Need any help with your projects,

Want to set up a presentation to your group,

Would like to meet to see how we can help your team, and expand our business together,

Are looking for company information,

Please contact: Marisol Serrao, Principal at 617 263 8879 or mserrao@vermeulens.com.

Richard Vermeulen

Senior Principal

Blair tennant

Senior Principal

Joshua Silverman

Senior Project Manager