What if this is the Recession?

Recent Blogs

- The Feds New Normal

- Market Outlook Fed Watch Part 2

- Market Outlook Fed Watch

- The Bipartisan Infrastructure Plan and Construction Costs

- Total Benefit - HVAC

- Steel Industry Volatility, Risks & Risk Mitigation

- The Ins and Outs of Insulated Concrete Forms

- Mini Construction Market Update

- How Do You Price an Elephant

- Where Did All the Wood Go

The great moderation was a period of disinflation spanning three decades through the 1980s to 2000s characterized by successive lowering of inflation rates, financial sector deregulation, boom and bust financial cycles, and deep recessions. Since the financial crisis, the world and the United States, in particular, have implemented a financial sector regulatory framework that controls money supply growth through numerous stress tests and mechanisms.

Long considered a panacea, a closely monitored financial sector could be structured to allow sequences of growth spurts and plateaus that avoid the lost opportunity of damaging recessions and catastrophic depressions.

With this in mind, we can look at the July 31st press conference with the Chairman of the Federal Reserve.

“We decided today to lower the target for the federal funds rate by a ¼ percentage point to a range of 2 percent to 2¼ percent. The outlook for the U.S. economy remains favorable, and this action is designed to support that outlook. It is intended to ensure against downside risks from weak global growth and trade policy uncertainty, to help offset the effects these factors are currently having on the economy, and to promote a faster return of inflation to our symmetric 2 percent objective. All of these objectives will support the achievement of our overarching goal: to sustain the expansion, with a strong job market and inflation close to our objective, for the benefit of the American people. We also decided to conclude the runoff of our securities portfolio in August rather than in September, as previously planned.”

This means that both trajectories of interest rate and quantitative tightening have been replaced by interest rate reduction and a hold on the quantitative money supply.

“…weak global growth (particularly in Europe and China) and trade tensions (at times disruptive and then less so) are having an effect on the U.S. economy. You see weak investment, you see weak manufacturing—so support demand there and keep that outlook favorable… The mechanical effects of tariffs are quite small. The real question is, what are the effects on the economy through the business confidence channel? I’ve seen some research, which indicates meaningful effects on output.”

This means that the capital marketing leveling through 2018 and 2019 has run its course and there is room for stimulus, particularly with respect to confidence levels.

“…we are getting lots of feedback from people who work and live in low to moderate-income communities to the effect that they’re now feeling the recovery, and they haven’t felt a better labor market in anybody’s memory… the best thing we can do for those people is to sustain the expansion, keep it going, and that’s one of the overarching goals of our policy moves. There really is no reason why the expansion can’t keep going. Inflation is not troublingly high… there’s no sector that’s booming and therefore might bust. You have a well-balanced economy… the engine, though, is really a consumer economy, which is 70 percent of the economy. The manufacturing economy—the investment and manufacturing part of the economy, is not growing much. It’s at a healthy level but not growing much.”

This means that the labor pool is expanding to reach a large segment of marginally productive people. Bringing these people into the “haves” of society is something new to the mandate of the central banks. In previous expansions, a low unemployment rate would trigger inflation and monetary tightening, leaving an underclass of people dependent on government programs.

“…we have a financial stability framework now for the first time. Before the crisis, we didn’t have this, but now we have it, and we publish it. We look at four big things so that the public can hold us accountable because it’s transparent. The first thing is valuation pressures, and we do see notable valuation pressures in some markets but not at a highly troubling level. Household and business borrowing are the second thing. Household borrowing is in very good shape overall. Leverage in the financial system is low, and funding risk is low. The place that gets a lot of attention—is business borrowing. What’s happening with business borrowing is, the loans have moved off the balance sheets of the banks and into market-based vehicles, which tend to be stably funded. But, nonetheless, it’s clear that the highly leveraged business sector could act as an amplifier to a downturn. So we’re watching that very carefully. The U.S. financial system, what you see is a high level of resilience—much higher than it was before the crisis—and that gives us the ability to use monetary policy for its purposes and rely on supervisory and regulatory tools to keep the financial system resilient.”

This means that regulatory tools, not interest rates, will be used to manage high debt levels in the business sector. This is more of a surgical approach to risk management that was not available to regulators prior to the financial crisis. Fix the problems where they exist rather than put the entire economy into a freeze.

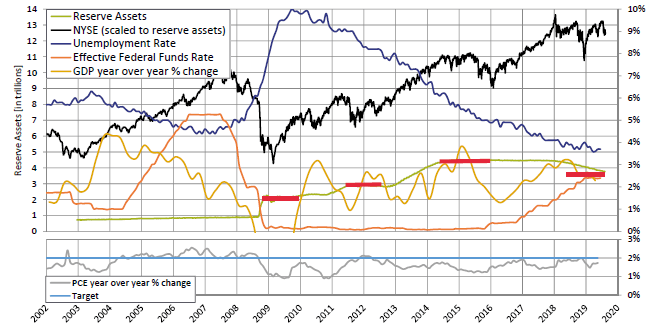

Below is our Market Outlook Quarterly chart of Federal Reserve Indicators highlighting the rise and plateau cycles of the post-financial crisis era. With interest rates near zero, the Fed used quantitative easing to stimulate the financial sector and support the economy. As the economy recovered, the Fed was able to end quantitative easing and raise interest rates to moderate growth (GDP), inflation (Personal Consumption Expenditures), and valuations (New York Stock Exchange).

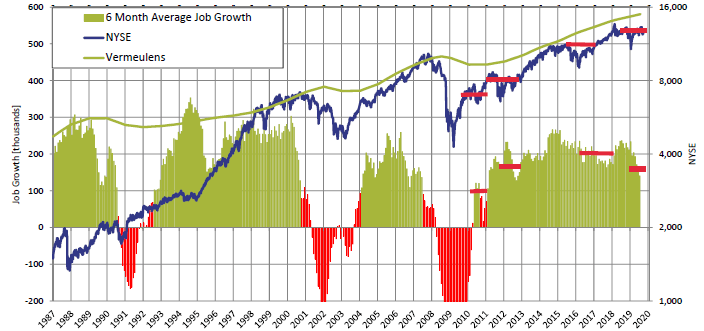

Below is our Market Outlook Quarterly chart of US Job Growth highlighting the rise and plateau cycles of the post-financial crisis era in contrast to the boom and bust cycles of The Great Moderation. If this pattern continues, we will be talking about “growth recessions” more and true recessions (two-quarters of falling GDP), hopefully, less.

Richard Vermeulen

Senior Principal

Richard has been in the industry for over 3 decades. He is the

creator of the Quarterly Market Outlook and chairs the Vermeulens Forum.

Previous Blogs